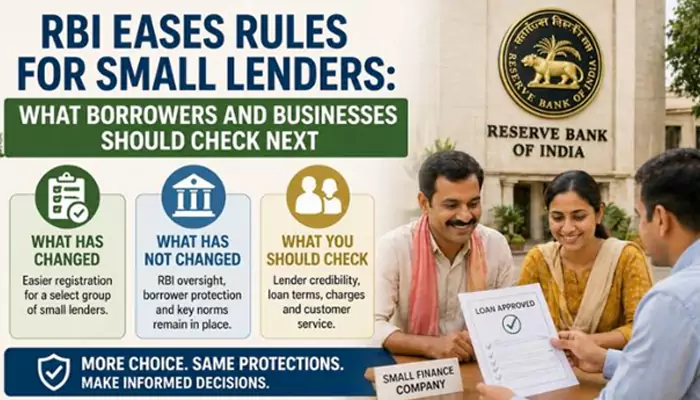

RBI Eases Rules For Small Lenders: What Borrowers And Businesses Should Check Next

- Devyani

- 3 months ago

- 3 minutes read

The Reserve Bank has relaxed registration rules for a narrow group of small finance companies, but borrowers and businesses should know what has changed, and what has not.

The Reserve Bank of India has eased rules for a specific category of small non-banking finance companies. These are companies with assets below ₹1,000 crore, no public funds, and no customer interface. From July 1, 2026, they will be exempt from registration and reserve-fund requirements under Sections 45IA and 45IC of the RBI Act. Existing eligible entities can apply for deregistration by December 31, 2026.

That sounds technical, and yes, it is. But the layperson’s translation is simpler: RBI is reducing paperwork for small finance firms that do not raise public money and do not deal directly with customers.

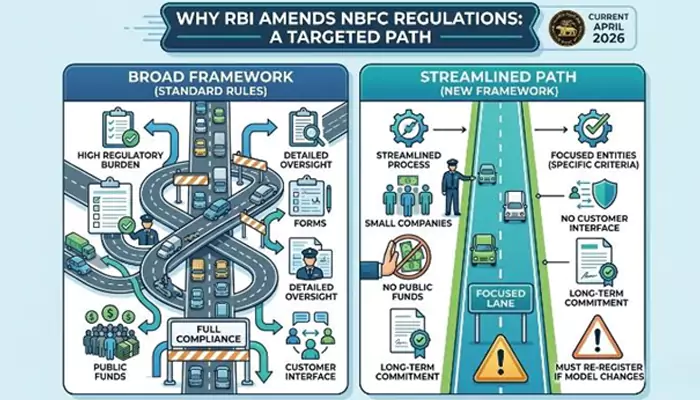

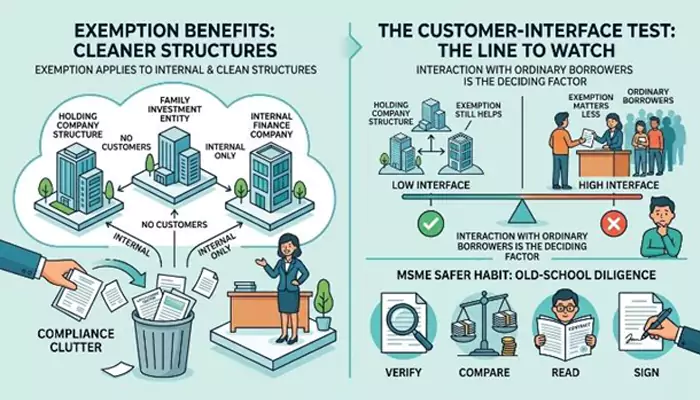

Why RBI Is Doing This

The change follows a review of the regulatory framework for companies that neither use public funds nor interact with customers. RBI’s amendment says such entities must operate without public funds and customer interface as a conscious, long-term business model.

In plain English, this is not a free pass for every small lender. It is more like a smaller lane at a toll plaza for vehicles that clearly fit the lane. If the company starts using public funds or dealing with customers, it must seek the proper registration again.

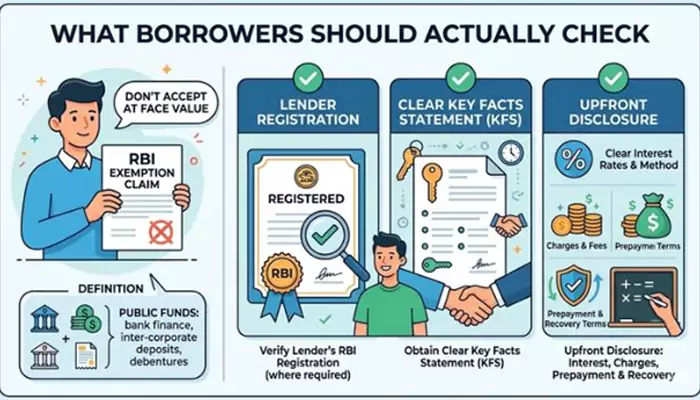

What Borrowers Should Actually Check

Here is the practical bit. If a company is offering loans directly to you, claiming “RBI exemption” should not be accepted at face value. RBI’s own FAQ says public funds are broader than public deposits and can include bank finance, inter-corporate deposits, commercial papers and debentures.

Borrowers should still check three things: whether the lender is RBI-registered where required, whether the loan has a clear Key Facts Statement, and whether interest, charges, prepayment rules and recovery terms are disclosed upfront. RBI says NBFCs must communicate interest rates and the method of arriving at them clearly to borrowers.

What Businesses Should Watch

For small businesses, the change may quietly help cleaner holding-company structures, family investment entities and internal finance companies that do not face customers. Less compliance clutter can be useful. Nobody opens a business dreaming of forms and reserve transfers, honestly.

The novel angle is the “customer-interface test.” That is the line to watch. The more a finance company faces ordinary borrowers, the less this exemption should matter to them. For MSMEs seeking credit, the safer habit remains old-school: verify, compare, read, then sign.

RBI’s move is a compliance relief, not a blanket lending reform. Borrowers should remain alert, while businesses should track whether their finance partners are customer-facing, fund-raising, or genuinely covered by the exemption.

.webp)

.webp)

.webp)

.webp)