A New Post Office Bank Account For Women’s Groups: What Members Should Check Before Joining

- Devyani

- 9 hours ago

- 3 minutes read

India Post Payments Bank’s new savings account gives women-led self-help groups a low-cost banking route. The useful part is not just “zero balance”, but doorstep access and cleaner group money records.

Sometimes, the biggest banking update is not a shiny app. It is a postman turning up with a device, a form, and the patience to explain things properly.

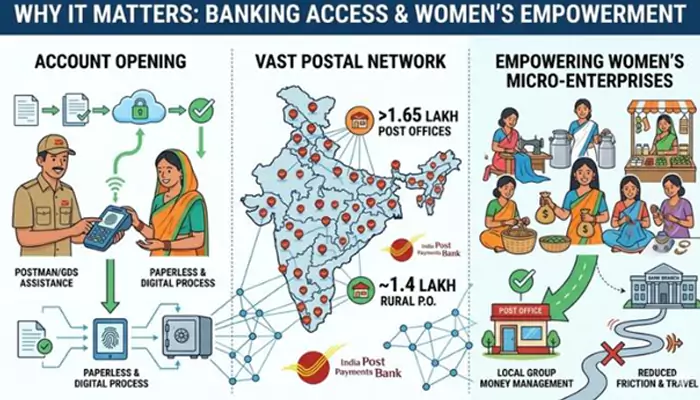

India Post Payments Bank, a 100% Government of India-owned bank under the Department of Posts, launched a new Self-Help Group Savings Account on April 30 at 3:15 PM. The account is meant for women-led rural self-help groups that need a simpler way to keep group savings, deposits and withdrawals inside the formal banking system.

What Members Get

The account has been designed as a zero-balance, zero-charges product. There is no minimum initial deposit and no monthly average balance requirement. The maximum balance limit is ₹2,00,000, with quarterly interest payouts as per applicable savings rates. Cash deposits and withdrawals are free, and groups also get one free physical account statement every month.

That sounds small, but for many groups, small charges are not small. They become irritation, confusion, and sometimes arguments in the monthly meeting. Who paid what? Why was this amount cut? You know the scene.

Why It Matters

The sharper story is access. India Post Payments Bank says the account can be opened through a paperless, digitally enabled process, assisted by postmen or Gramin Dak Sevaks. Banking support is also linked to India’s postal network of more than 1.65 lakh post offices, including about 1.4 lakh in rural areas.

For women’s groups involved in tailoring, dairy work, small trading, handicrafts, embroidery, artificial jewellery or other local micro-enterprises, this could reduce the familiar friction of travelling to a branch just to manage group money.

The Fine Print To Check

Members should still ask practical questions before opening the account. Who will operate it? How will withdrawals be approved? Where will the passbook or statement be kept? What happens if the group crosses the ₹2 lakh balance cap?

Also, some services are not available with this account: mobile banking, nomination facility, POSA account linkage, standing instructions, bill payments, mobile recharges and virtual debit card issuance. That is not necessarily a deal-breaker, but it should be known before the first deposit.

The Bigger Picture

India’s self-help group ecosystem is already massive. As of December 2025, 10.05 crore households had been mobilised into 90.91 lakh self-help groups under the National Rural Livelihoods Mission.

The novel point is this: the account may work best as a group cashbook with banking rails. Not glamorous. Useful. If members use statements carefully, it can make trust, repayments and small-business planning easier.

For women’s self-help groups, this account is worth checking, especially where bank branches are far or charges create confusion. The next step is simple: compare features, assign operators clearly, and keep records clean from day one.